How to Prepare for Tough Times

I was whining yesterday to my wicked smart friend Mina Ratkalkar (sex therapist, forensic psychologist, and consent expert) that I had no newsletter ideas. She bailed me out by texting the following:

Mina’s suggestion came on the heels of being invited to speak at a Recession Rx Your Money event hosted by another buddy, medical money guru Latifat Akintade, MD.

It’s clearly time to tackle the scary financial headlines in everyone’s doomscrolling feed.

As if Putin threatening to go nuclear, our planet being a dumpster fire, and the continued trampling of human rights weren’t enough, the financial overlords appear to have fucked things up.

Not going to point fingers here because global finance is way too complicated for a simple “The butler did it” Agatha Christie-style villain. And even if we could blame one person/entity/thing, how would that be helpful?

Likewise, being too prescriptive is not the answer. I don’t want you to turn into a financial survivalist hunkering down in your bunker, waiting for the apocalypse to come. That’s no way to live.

It’s important to remember that crisis also creates opportunity.

So here are some recommendations that will prevent panic and paralysis, allowing you to find the silver lining in financial storm clouds looming over the horizon.

But first, a story.

My grandfather, as a 16-year old hayseed from Tennessee, arrived in New York in 1897 and became a runner (messenger boy) on Wall Street for the brokerage firm DeCoppet and Doremus. Fun fact: Hollywood legend Douglas Fairbanks was a fellow runner and roommate.

Grandaddy went to NYU law school at night and was the valedictorian of the 1906 graduating class. He passed the bar but never practiced law, continuing his career on Wall Street. In 1911 he bought a seat on the New York Stock Exchange and, by the late 1920s, became a partner in DeCoppet. He was superb at “reading the tape” and his point of view is well worth sharing with you:

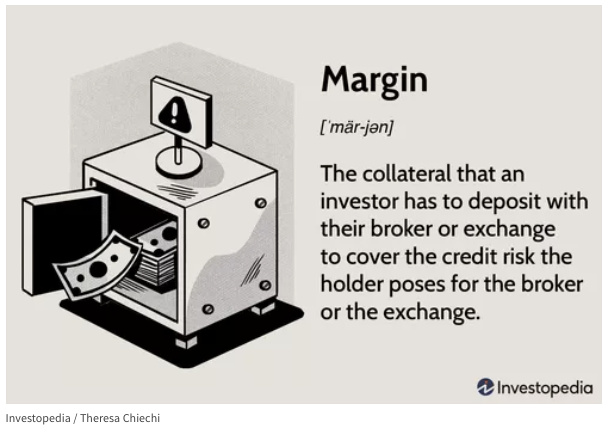

Granddaddy believed you should never buy stock on margin.

When the market crashed on October 29th, 1929, my grandparents were in Europe (they loved to travel) and carried on as though nothing had happened. Because they didn’t owe any money, they were able to help out relatives and made it through the Great Depression relatively unscathed.

The investors who didn’t were the ones who’d borrowed money and didn’t just lose what they had; they also lost what they borrowed.

Later in the 1930s, his friends Albert (a fellow bridge player and stockbroker) and Maggie Rudkin approached Grandaddy for a $5,000 loan.

Rudkin needed capital for her specialty bread business. My grandfather thought selling premium-priced bread during the Depression was not a surefire business idea. He thought the business would fail but didn’t want to ruin their friendship over a debt he was sure could not be repaid. So he offered to invest, rather than lend the money, in exchange for a 10% stake. That way, if her company failed, there would be no question of repayment.

(I’ll table the discussion on debt vs. equity, power dynamics, and minority ownership for another newsletter.)

Well, Maggie Rudkin was a badass and a hell of a businesswoman, way ahead of her time. (A future newsletter topic.) Her specialty bread company, Pepperidge Farm, first developed to cater to her son’s allergies, was sold to Campbell soup twenty years later for $27,000,000.

(Don’t get too excited. My father managed to piss away completely his share of the windfall in failed business ventures, but that’s for yet another issue.)

My family stories contain important lessons for how to prepare for financial ill winds that may be a-comin’.

Too much leverage (debt) is deadly in tough times

For one, the income to carry that debt risks drying up, leaving you with having to pony up more cash.

Say you borrowed money to buy a building that you are renting out. Your tenants have hard times and can’t pay you. It’s hard to attract other tenants because when people are queuing up in bread lines, they’ve got bigger problems. So you either have no rental income or take in less than your carrying costs – taxes, insurance, maintenance, and mortgage.

You’re bleeding cash, and if you don’t have it, it’s a big problem. You end up unloading the building at a fire sale price, wiping out whatever equity you had in the place, and still owing the bank a shit ton of money.

What’s worse?

Swift financial death from borrowing to own volatile financial assets – stocks, commodities, futures, options, or crypto. If you can’t put up more cash, the brokerage firm will sell your positions out from under and you will get bupkis. That’s Yiddish for big fat zero.

Leverage is your friend when asset prices are going up, but it is deadly in a downturn.

So take risk off your balance sheet by making sure you stress test the debt you have. What happens when the income that supports it plunges by 20%? 50%?

Pay debt down to a level that will let you sleep at night.

Remember that LIQUIDITY is critical here. In a financial meltdown, you don’t want to be asset rich via leverage but cash-poor.

In a downturn, credit becomes tight. No one wants to or has the capital to lend in a crisis. And those that do won’t be generous with their terms, given that both interest rates and credit risk are high.

Hence the old truism that banks only want to lend you money when you don’t need it. (Not strictly true BTW and a subject for a future newsletter. Not going to run out of ideas any time soon, I guess!)

Properly deployed, debt (leverage) is a great financial tool, deadly if it’s not.

Ahead of Her Time

Rudkin’s innovations weren’t strictly in the culinary realm. Before the advent of second-wave feminism, she was encouraging women to work and hiring them to acclimate the American public to the very idea of women in the workplace.

In the early 1940s, she was offering “sound advice for other women who want to go into business for themselves,” inspiring an article titled “We, the Women,” which bemoaned that the business world would not hire women despite the capabilities they demonstrated in managing the home.

Rudkin also hired housewives in the early days of her baking operation. “Look at what a bunch of women over 40 have done,” she told the AP in 1943 of the 125 women working in her bread bakery. “None of us had training or business experience. Most of us have children and home responsibilities. But we’re running this business and making it pay.”

Source: “The Remarkable Life of Margaret Rudkin, Founder of Pepperidge Farm” by Mari Uyehara

Look for the opportunities that emerge from upheaval

Never mind that Grandaddy made a great investment by happenstance. I’m sure he read the financials, but he was investing in the Rudkins despite his judgment that a high-priced specialty bread business was sure to fail.

Nevertheless, the business OPPORTUNITY was still there:

“She (Maggie Rudkin) attributed its (whole wheat specialty bread) success to a combination of “quality and timing”—with the advent of commercial food products, women had stopped making bread at home, but there was nothing at the level of homemade in the grocery stores yet.”

— “The Remarkable Life of Margaret Rudkin, Founder of Pepperidge Farm”

There is ALWAYS opportunity.

The world is always changing, but at times of upheaval, it changes even faster and in a more chaotic way, giving countless opportunities to those nimble, visionary, or passionate enough to seize them.

So don’t let fear blind you to opportunities.

The pendulum of change swings back and forth – not always in a perfect arc – but human matters have a way, like all complex systems, of eventually reaching some kind of homeostasis.

Extremes are exhausting to maintain.

Other opportunities that may present themselves:

When times are tough, everything is negotiable.

Terms become more flexible. Your patronage becomes valued and pursued. You can afford to be choosier, upgrade your vendors, and negotiate better terms.

Keep investing your long-term “mattress” money.

If you can, add more to the amount you sock away because its buying power is amplified when the market is on its ass.

The only sale we don’t like is when equities are being discounted.

Stay invested. It’s impossible to time the market, and because the market has an upwards bias over the long haul, missing the big up days will cost you a lot in compounded returns over the years.

NO ONE knows what the market will do or when the market will bottom (it always bottoms BEFORE the world bottoms), though lots of talking heads will pretend to. Those that actually make the right call, whether by dint of good research, superb instincts, or just dumb luck, may not be right the next time.

Be skeptical of anyone who tells you they have the magic formula.

Money you don’t have to touch for decades should be aggressively invested, but in a dollar-cost averaging way, because no one can time it perfectly, even the “experts”.

Even in bear markets that last a long time, there are sharp rallies.

Stay the course, ESPECIALLY if you are young and have an enormous timeline.

Seriously.

My young friends, invest whatever you can spare and let time and compounding make you rich. It’s so easy now to put small amounts to work inexpensively. Make it habit. Better yet, make it a game. (I sense another newsletter brewing.)

If you, like me, are in your wisdom years, the answer is too nuanced to address here. Bear markets can last longer than our life expectancy.

Just be open to possibilities and opportunities.

You can only be open-minded and curious when your brain is not shut down in fear. Back to my first point about leverage.

Manage your debt and have enough liquidity so you don’t get in a jam. You might come out of this downturn having made brilliant investments, even if, like my Grandfather you do it for the “wrong” business reasons (equity is far riskier than debt) but the “right” reasons of the heart.

P.S.

I'll be teaching a class on Financial Intimacy for Business Owners this October. You’ll make better and more profitable business decisions when you approach your financials with curiosity and listen the stories they’re telling you. Sign up here for early bird notification.