Nearing Retirement? 3 Money Rules to Live By and Enjoy Your Golden Years

In the space of 2 days I got three flyers inviting me to learn more about retirement financial strategies. These were advertised as workshops and educational opportunities.

My sudden popularity made me deeply suspicious.

The invitations, from three different financial “advisors/planners/educators” violated all the rules of good design. A riot of colors, a cornucopia of font types and sizes, an admission “ticket” to be torn off, and my name emblazoned everywhere because I am a very, very special person.

Every direct-mail gimmick was used to lure me in.

This is an expensive marketing campaign – not only the snail mail was thick and glossy, but the meals themselves, at least judging from the food p*rn shown, weren’t going to be cheap. It had to be a sales pitch masquerading as education. No “workshop” or “educational seminar” without strings attached would spend this much dough to get butts in seats.

Money Rule #1: The more expensive the bait, the more valuable the fish

If it costs a lot to land a customer, it means there’s big money to be made once you’re hooked. Think about it. You’re less likely to think critically of your host when you’ve benefited from their hospitality. As humans, we’re wired to reciprocate kindness. Your goodwill, now fattened up, means you’ll say yes to the offer of a one-on-one meeting, where it’s even harder to say no to a sales pitch.

But here’s the thing – you don’t owe your host anything. That meal may cost them money, but it costs you time and attention. It’s a fair exchange. You did your part just by showing up.

I took a closer look at the people who invited me.

They all were selling insurance, but it was hard to tell, given the smoke and mirrors on their flyers, websites, and LinkedIn profiles where the word “insurance,” when found, needed a magnifying glass to be seen.

Money Rule #2: A lack of transparency implies monkey business

When there’s a hidden agenda, assume a nefarious purpose. Here’s a sampling of what I heard at dinner:

A “Certified Financial Fiduciary” was touted as being the equivalent of “having an alphabet soup” (e.g. CFP for Certified Financial Planner, CFA for Chartered Financial Analyst) after their name. It’s so not. Pay attention to credentials. While they won’t guarantee ethics or competency, they skew the odds towards them.

The absence of relevant biographical details (i.e. education, credentials, experience) amidst lots of “I love to fish, eat pineapple pizza and play with my dogs” type of personal details was notable. They want you to like them and to be treated like family, not to be assessed for credibility.

One firm had multiple locations listed as though they were a giant financial services firm. Turns out there were no locations at all, just that staff lived in different places. Not to mention their website did not even mention their NAMES, let alone have bios. It’s as if they’re on the lam. Who are they hiding from?

Let me clear. My beef is not with insurance.

My first job in financial services was as a retirement benefits counselor at TIAA-CREF (Teachers’ Insurance and Annuity Association and the College Retirement Equity Fund). This Fortune 100 company with $1 Trillion in assets was founded by Andrew Carnegie to provide insurance and retirement products to teachers, professors and other non-profit professionals. It’s a non-profit created for a philanthropic purpose. I loved learning about pensions, retirement planning, and insurance, and speaking to our customers.

I believe insurance, properly deployed, is human financial ingenuity at its best but, in the wrong hands becomes a weapon of financial mass destruction.

Given the amount of fog I was having to navigate just researching who sent me the flyers, I was pretty sure which I would encounter if I accepted their invitation.

Dear reader, I took one for the team.

I signed up for two dinners, and was waitlisted for the third — spots are limited! (Note their use of FOMO and urgency.)

Despite my cynical decades on Wall Street, I may still be more naive and gullible than the average bear. Why else would I be so… SCANDALIZED …by what I heard:

Half-lies

Full-blown whoppers

Fear-mongering scare tactics and

Psychological manipulation worthy of a hostage negotiator or CIA interrogator.

For one, the claim that insurance companies are bulletproof, unlike banks. The “financial educator” raised the specter of bank runs putting your nest egg at risk, omitting that there’s $250,000 of FDIC insurance (per depositor, per bank, per ownership category) backed by the full faith and credit of the U.S. government.

For another, the suggestion that insurance companies never go insolvent. 🙄 Not true.

My friend, if you don’t learn how to decode financial bullshit, you won’t stand a chance against these smooth operators.

They are pros at separating people from their money in the guise of guaranteed “safety.” They impugn everything and everyone else in the financial ecosystem so that by the end of the dinner, you feel like only they can save you from becoming broke in retirement.

According to the presenters, banks are unsafe, the market will maul you, inflation will eat you alive, and the taxing authorities will pillage your net worth.

The only salvation for a secure future (according to them)? Annuities.

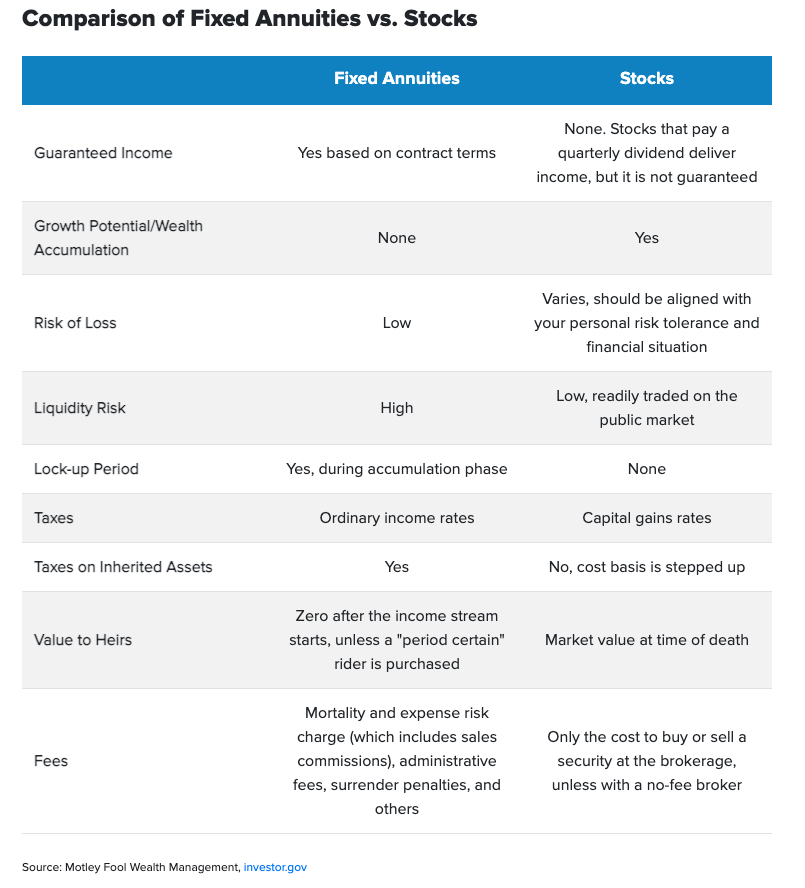

There are many kinds of annuities, but the short definition is they’re insurance contracts that guarantee a set income. They sell well in down markets when people are afraid of running out of money in retirement and overvalue downside protection.

2022 is on track to beat 2008, the industry’s peak sales year. No surprise – 2008 was an economic dumpster fire of a year. No one wants annuities when bull markets are roaring. That should tell you something. Fear drives their sale. Decisions made in fear are rarely rational.

In any case, that’s a lot of flyers, fear mongering, and “free” meals.

But annuities are tricky products, because sales commissions run from mid-single digits to double digits. For example: At a 10% commission, for every $100 you put in an annuity, the insurance company has to recoup $10 paid out in commission before it can make money — you pay for that acquisition cost one way or the other, typically in the form of lower returns.

In addition, upside (growth in your assets) is capped so you don’t benefit from up markets, and liquidity (getting your hands on your money whenever you want) is virtually non-existent.

My favorite line from dinner: “If you’ve heard of people having bad experiences with annuities it’s because they were sold the wrong annuity. There’s no such thing as a bad annuity, just the wrong annuity.” 🤣

Annuities can make sense for some people, in specific financial situations. It is not, no matter what the “financial educators” say, a retirement panacea.

There’s a time and a place for insurance and insurance products, but not when it starts with an expensive free meal and ends with fear mongering scare tactics.

In short: Buyer beware. ⚠️

Get started with this overview of Annuities:

Money Rule #3: There is no such thing as a free lunch

Ask what the commissions are: “For every dollar I pay into this annuity, what percentage is actually invested on my behalf?”

Ask: “Is the rate of return used here to illustrate what my income would be guaranteed to not change?” (It’s common for companies to advertise a high return as a teaser, and then lower it after a time.)

And don’t forget to apply Money Rules #1 and #2.